In my most recent blog post, I did a synopsis of the mobile money ecosystem in Africa which began to gain global attention with the launch of Kenya’s M-PESA (mobile money services) in 2007. To keep on topic in the money mobile ecosystem mini-series, let’s shift focus to another region, Asia. If you have not yet read the blog on Africa, you may do so here:

A quick fun fact! Records have shown that the first ever mobile money provider, SMART Money, was launched in the Philippines in 2001 and that by 2006, there were around six mobile services across four countries in East Asia and the Pacific region.

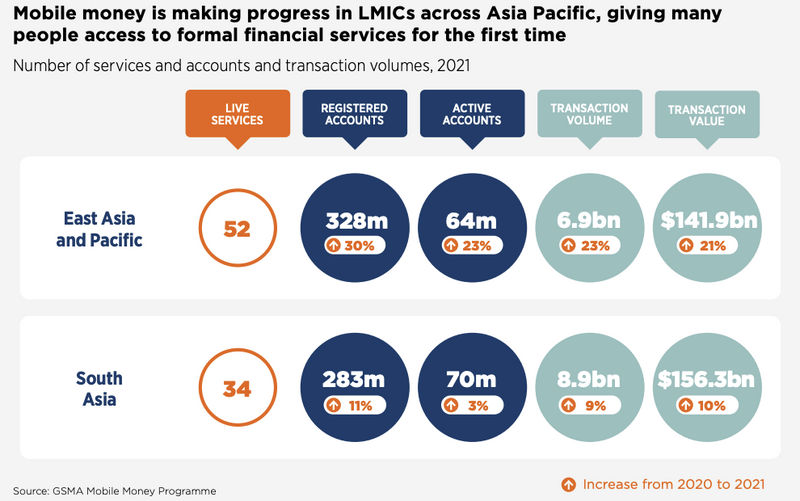

Asia has played and continues to play a major role in the development of the digital payments space and has pioneered advances for further financial inclusion with new developments and widespread adoption of digital identification. Asia has some of the most innovative countries that have since initiated country-wide digitization programs that have influenced high rates of adoption of digital solutions such as digital wallets, mobile payment apps, and the use of stored value cards. According to the GSMA’s Mobile Economy Asia-Pacific publication, the region has some 86 live money services with transactions valued at nearly $300 billion at the end of 2021.

Mobile Payment Revolution & Digital Identify

Mobile payment has proven to be successful across territories in Asia due to the unwavering support and accountability of the respective governments in providing enabling regulatory frameworks and the rollout of financial literacy initiatives. The bedrock of our current society where you make payment for services, send monetary gifts to those in need, and shop at local stores via QR codes, directly via your mobile.

One can argue that China has been at the helm of what is deemed as the mobile payment revolution. The enablers are pretty much the same across regions: increasing access to smartphones and improving access to the Internet. But what’s worthy to note in the Chinese context is that large firms outside of telecoms like Alibaba in retail (Alipay) and the social media giant WeChat (WeChat Pay) have charted the course in serving as intermediaries and are reducing the role of banks by enabling certain transactions.

The use of mobile phone numbers (and even national identification numbers) is driving cross-border transactions powered by domestic rails. Take Singapore (PayNow) and Thailand (PromptPay) as an example. Both nations have partnered with their respective national real-time payment systems to foster secured and fast cross-border payments.

In the Asia Pacific region, the role advances in digital identity have played in providing alternate access to individuals who don’t satisfy the Know Your Customer (KYC) regulations and are marginalized from traditional financial services has been tremendous. India’s Aadhaar program has created digital biometrics for approximately 1.3 billion Indians which then serves as the requisite, for those without a bank card, to attain access to the Unified Payments Interface (UPI), India’s real-time payment system facilitating transfers based on mobile numbers, across banks.

Despite the plethora of digital payment options available in Asia-Pacific territories, there still is some degree of the lack of interoperability among these systems inhibiting a full transition to cashless in some societies. Over the past decade, we’ve witnessed a wave of Asian fintechs having recognized the gaps in the digital payment space, and have charted the path to innovate smooth, interoperable systems. One such fintech is our grantee ThitsaWorks which is building a payment portal that seeks to build a bridge for microfinance institutions (MFIs) that lack core systems and/or API capabilities to connect to a Mojaloop-enabled payment switch. This will serve more than 2 million unbanked and underbanked in Myanmar immediately and has the potential to benefit up to 13 million in the future.

To find out more about the ThitsaWorks project, you may review their reports here:

Follow for the next synopsis of the mobile money ecosystem. Can you guess what region I'll be exploring next?

Top comments (0)